FREE FOR ARO READERS

What's your path to a

property-funded retirement?

Three free tools. One clear number. See exactly where you stand today, and what it actually takes to get where you're going.

$997

$0 (for a limited time only)

What you get instant access to

No cost, no catch — just the same tools we use with our own clients.

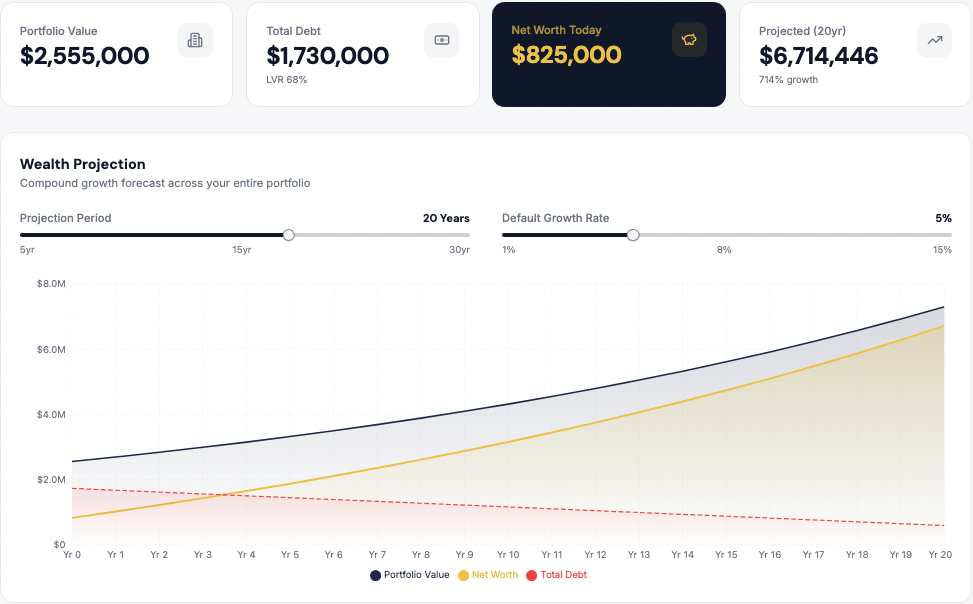

01 — NET WORTH

See your real net worth, projected 20 years out

Map your properties, debt and equity. Then watch what compounding actually looks like for your portfolio over the next two decades.

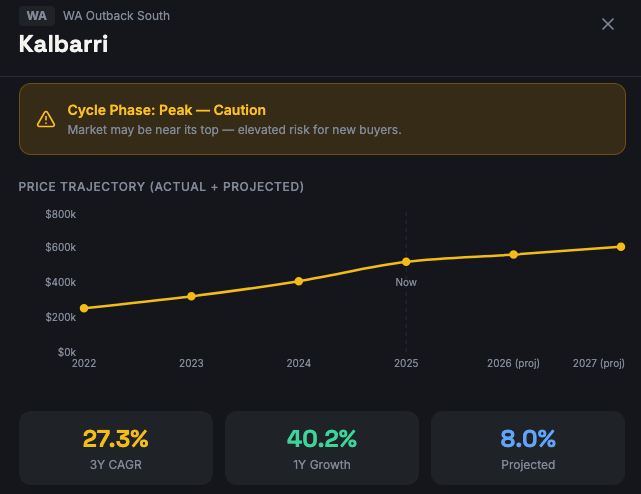

02 — SUBURB DATA

Find the suburbs already outperforming

An interactive heatmap covering 200 Australian suburbs with 3-year CAGR, cycle-phase, rental yield and vacancy data — updated April 2026.

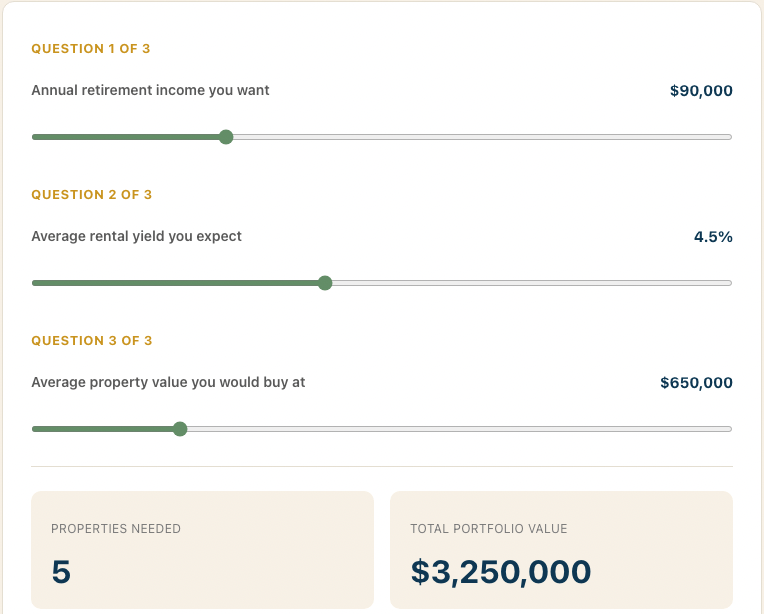

03 — YOUR NUMBER

Know exactly how many properties you need

Answer three questions and find out exactly how many properties — and what portfolio value — it takes to retire on your terms.

Get instant access — it's free for a limited time only

Enter your details and we'll send access to all three tools immediately.

No spam. Unsubscribe anytime. Takes 30 seconds.

Three tools, ready the moment you sign up

All three included free, with no time limit.

TOOL 01 — PROPFOLIO

Property Net Worth Tracker

Add your properties, set your growth assumptions, and see your portfolio value, equity, LVR and projected net worth — out to 30 years. Built for Australian investors.

TOOL 02 — SUBURB PULSE

Growth Intelligence Tool

Search any of Australia's top 200 suburbs and instantly see 3-year CAGR, growth, cycle phase, median price, rental yield and vacancy rate — updated regularly.

TOOL 03 — YOUR NUMBER

Property Number Calculator

Answer three quick questions about your income goal, savings and timeline, and get an instant estimate of how many properties — and what portfolio value — it will take to retire on your terms.

Australian Retirement Office | ausretirementoffice.com.au

General information only — not financial advice. No AFSL held.

Enter your details for immediate access to the Investor Toolkit

We HATE spam. Your email address is 100% secure